Practical disposable transfer pipettes, made from natural low density polyethylene (LDPE). The transfer pipet is simple and safe to use with a long shelf life; no issues with broken glass, cracked or loose bulbs. Additional advantage is that with the single piece design lager amount can be transferred by allowing fluids in the bulb. These plastic transfer pipettes are ideal for transferring small amounts of fluids for microscopy sample preparations or to prepare mixtures or staining solutions. The extra fine tip enables transferring minute amount of fluids. These cost-efficient plastic transfer pipettes are disposable and intended for one-time use. Ideal for educational and research environments. Can be used for fluids up to 70°C, please take care to protect the fingers squeezing the bulb. Available in six sizes/styles: 0.5ml, 1ml, 2ml, 3ml, 5ml, 10ml.

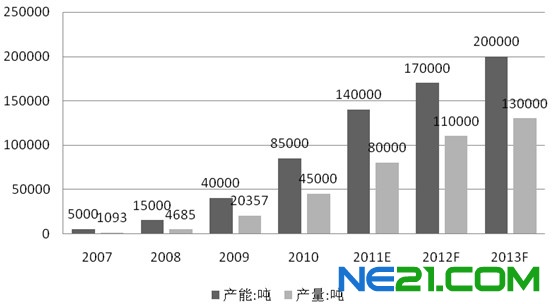

Plastic Transfer Pipettes,Disposable Transfer Pipettes,Sterile Transfer Pipettes,Disposable Plastic Pipettes,3ml Pipette,5ml Plastic Pipette,Pasteur Pipettes Yong Yue Medical Technology(Kunshan) Co.,Ltd , https://www.yongyuetube.com Figure 1 China's and global solar cell production growth is affected by changes in the international PV market. China's polysilicon industry has experienced a rapid development of the "bubble period" from 2005 to 2008, and also experienced the "downturn" after the 2008-2009 financial crisis. . From 2010 to 2011, with the further fluctuation of the global photovoltaic industry, China's polysilicon industry and market are gradually adjusting to maturity. In 2010, China's polysilicon production reached 45,000 tons, doubled from 22,000 tons in 2009, with annual sales exceeding 23 billion yuan and total employment exceeding 15,000. In 2011, domestic polysilicon production is expected to exceed 80,000 tons, and the production capacity will reach 140,000 tons. By the end of the "Twelfth Five-Year Plan", China's polysilicon production capacity will reach 200,000 tons. Domestic polysilicon enterprises, such as Zhongneng Silicon, Jiangxi LDK, Luoyang Zhongsi, Daquan Group, etc., have already reached the forefront of the world.

Figure 1 China's and global solar cell production growth is affected by changes in the international PV market. China's polysilicon industry has experienced a rapid development of the "bubble period" from 2005 to 2008, and also experienced the "downturn" after the 2008-2009 financial crisis. . From 2010 to 2011, with the further fluctuation of the global photovoltaic industry, China's polysilicon industry and market are gradually adjusting to maturity. In 2010, China's polysilicon production reached 45,000 tons, doubled from 22,000 tons in 2009, with annual sales exceeding 23 billion yuan and total employment exceeding 15,000. In 2011, domestic polysilicon production is expected to exceed 80,000 tons, and the production capacity will reach 140,000 tons. By the end of the "Twelfth Five-Year Plan", China's polysilicon production capacity will reach 200,000 tons. Domestic polysilicon enterprises, such as Zhongneng Silicon, Jiangxi LDK, Luoyang Zhongsi, Daquan Group, etc., have already reached the forefront of the world.  Figure 2 Domestic polysilicon capacity production growth trend Since the beginning of 2011, many European countries have suffered from the European debt crisis, and they have lowered their PV subsidies. The demand for photovoltaic market has gradually deteriorated, the inventory of photovoltaic products has been severe, and prices have been falling. The shrinking demand in the terminal market, coupled with the release of polysilicon production capacity at home and abroad, has led to a decline in the price of polysilicon products, from 80 US dollars/kg at the beginning of the year to the current 30 US dollars/kg, a drop of 60%. Foreign polysilicon companies, such as OCI and Hemlock, continue to cut prices and hit the domestic polysilicon market. At present, some polysilicon enterprises with small production capacity and high cost in China have faced a survival balance point due to the current market price, which is higher than the production cost. Some enterprises have stopped production or reduced production.

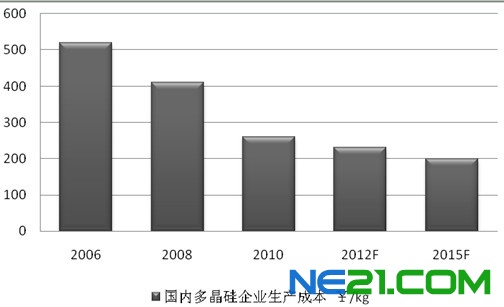

Figure 2 Domestic polysilicon capacity production growth trend Since the beginning of 2011, many European countries have suffered from the European debt crisis, and they have lowered their PV subsidies. The demand for photovoltaic market has gradually deteriorated, the inventory of photovoltaic products has been severe, and prices have been falling. The shrinking demand in the terminal market, coupled with the release of polysilicon production capacity at home and abroad, has led to a decline in the price of polysilicon products, from 80 US dollars/kg at the beginning of the year to the current 30 US dollars/kg, a drop of 60%. Foreign polysilicon companies, such as OCI and Hemlock, continue to cut prices and hit the domestic polysilicon market. At present, some polysilicon enterprises with small production capacity and high cost in China have faced a survival balance point due to the current market price, which is higher than the production cost. Some enterprises have stopped production or reduced production.  Figure 3 Decline in polysilicon prices in 2011 Progress in domestic polysilicon technology China's polysilicon industrialization technology continues to improve. In recent years, the global photovoltaic market has driven China's polysilicon industry to develop rapidly. On the basis of doubling the capacity production scale, the company has accumulated through its independent research and development, foreign advanced technology introduction and digestion and absorption, and has accumulated in production practice. And mastered the key technology of the large-scale production of the Siemens method, large-scale industrial production of polysilicon has been formed, which has a great impact on the global polysilicon industry structure. Compared with the initial level of the “Eleventh Five-Year Planâ€, domestic polysilicon production enterprises have greatly improved their production energy consumption and production costs. The average comprehensive energy consumption and reduction energy consumption are more than 300kWh/kg and 200kWh from 2006 to 2007 respectively. /kg or so, down to 160kWh/kg and 80kWh/kg in 2010, the energy consumption dropped by nearly 50%. The production cost has also dropped from the initial 70 US dollars / kg to the current 30 ~ 40 US dollars / kg, the production costs of some polysilicon enterprises have been reduced to 20 ~ 25 US dollars / kg, can compete with the international advanced enterprise level.

Figure 3 Decline in polysilicon prices in 2011 Progress in domestic polysilicon technology China's polysilicon industrialization technology continues to improve. In recent years, the global photovoltaic market has driven China's polysilicon industry to develop rapidly. On the basis of doubling the capacity production scale, the company has accumulated through its independent research and development, foreign advanced technology introduction and digestion and absorption, and has accumulated in production practice. And mastered the key technology of the large-scale production of the Siemens method, large-scale industrial production of polysilicon has been formed, which has a great impact on the global polysilicon industry structure. Compared with the initial level of the “Eleventh Five-Year Planâ€, domestic polysilicon production enterprises have greatly improved their production energy consumption and production costs. The average comprehensive energy consumption and reduction energy consumption are more than 300kWh/kg and 200kWh from 2006 to 2007 respectively. /kg or so, down to 160kWh/kg and 80kWh/kg in 2010, the energy consumption dropped by nearly 50%. The production cost has also dropped from the initial 70 US dollars / kg to the current 30 ~ 40 US dollars / kg, the production costs of some polysilicon enterprises have been reduced to 20 ~ 25 US dollars / kg, can compete with the international advanced enterprise level.  Figure 4 Trends in energy consumption of domestic polysilicon producers from 2007 to 2010

Figure 4 Trends in energy consumption of domestic polysilicon producers from 2007 to 2010  Figure 5 The decline in domestic polysilicon production costs The environmental protection of domestic polysilicon production is also a major concern of enterprises and the community. Improved Siemens process polysilicon production in the process (such as chlorosilane synthesis, reduction, hydrogenation, etc.), will be accompanied by the production of large amounts of hydrogen, hydrogen chloride, trichlorosilane and silicon tetrachloride, the main by-product is silicon tetrachloride , hydrogen chloride, hydrogen, and high and low boilers. From the current situation of China's polysilicon industry, the use of polysilicon production by-products has become an important part of the large-scale production of polysilicon. There are many ways to treat by-product silicon tetrachloride. The effect of its outlet or comprehensive utilization is directly related to the economic benefits, energy consumption and environmental protection of polysilicon production, and even directly threatens the normal operation of polysilicon production line. Moreover, the recycling of silicon tetrachloride, hydrogen chloride and hydrogen in by-products is generally beneficial to reduce production costs. For the recycling of silicon tetrachloride, from the current layout of domestic enterprises, it is more suitable to use hydrogenation treatment, which is converted into trichlorosilane and reused, which not only solves the emission problem, but also improves the production of polysilicon. Out. At present, most of the domestic enterprises are mainly based on high-temperature hydrogenation, and they are also actively researching and applying low-temperature hydrogenation. The enterprises represented by low-temperature hydrogenation and hydrochlorination include Luoyang Zhongsi and Xuzhou Zhongneng. At present, polysilicon enterprises that have been put into production in China, such as Xuzhou Zhongneng, have solved the problem of full material circulation and clean production, and some are in the process of being solved, but the projects with a capacity of more than 1000t are basically equipped with silicon tetrachloride hydrogenation unit and hydrogen chloride and hydrogen. recycling system. At present, some enterprises have not yet achieved full-closed production, mainly through export, comprehensive utilization and pollution-free treatment. It is necessary to speed up the improvement and strengthen further technological upgrading. On the whole, the technical level of domestic enterprises is still uneven, and the pressure of energy conservation and emission reduction and cost reduction still exists. Faced with increasingly severe international competitive pressures, further reduction of production costs through technological innovation, transformation and upgrading is an important issue facing domestic polysilicon enterprises. Main problems and suggestions for the development of domestic polysilicon industry In the past few years, high-purity polysilicon preparation technology has been monopolized by foreign countries, resulting in scarcity of raw materials, and prices have remained high for a period of time, attracting a large influx of domestic funds and enterprises. Objectively Promoted the development of the domestic polysilicon industry. However, the recent silicon material market is sluggish, prices continue to fall, and the low-cost competition of foreign polysilicon enterprises continues to impact. The polysilicon enterprises that have just grown up in China are facing the challenges of internal and external troubles. Promoting technological progress with independent innovation of enterprises and accelerating product structure adjustment may help solve development problems. 1 Actively cultivate the domestic market, domestic demand drives industrial development. China is the world's largest producer of solar cells, and its battery output accounts for more than half of the world's total output. However, more than 95% of domestic PV products rely on export to European and American markets. Once the European and American markets fluctuate, they will affect domestic upstream enterprises. Serious dependence on external demand is a fatal injury to the development of the domestic PV industry chain. The growth rate of the European and American markets slowed down. The contradiction between the imbalance of supply and demand in the domestic PV industry was immediately highlighted, and there was a large backlog of inventory. The fierce price wars of various manufacturers have seriously weakened the profitability of Chinese enterprises. With the successive introduction and implementation of national golden solar engineering and concession bidding projects, the start-up speed of China's photovoltaic market is gradually accelerating. In 2010, China's new PV installed capacity was 500MW, and the cumulative installed capacity reached 800MW, nearly double the year-on-year. . In 2011, the National Development and Reform Commission issued and implemented a subsidy policy for on-grid tariffs for photovoltaic power generation. The photovoltaic market has grown substantially. It is expected that the installed capacity of new PV in China will reach 2.5GW, a year-on-year increase of 400%. According to another report, China's solar power generation "Twelfth Five-Year Plan" will also increase the 2015 PV installation target from 10GW to 15GW, and will reach 50GW in 2020. All kinds of good news show that China's PV market will accelerate and expand, and the digestive capacity of domestic PV production capacity will continue to increase. Then, through the industry consolidation, those low-competitive backward production capacity will be eliminated. By then, the domestic market share will increase rapidly. Relieve corporate pressure. 2 Strengthening the guidance of industry norms and promoting the industry's high profit, high subsidy and other industry advantages before the self-discipline development of the industry, so that a large number of enterprises are eagerly awaiting, although objectively promoting the rapid development of the industry, but under the influence of market fluctuations, the domestic polysilicon project has no The negative phenomenon of the preface is revealed. The volatility of the photovoltaic market and industry has provided an opportunity for the integration and upgrading of China's polysilicon industry. The Ministry of Industry and Information Technology has issued the “Entry Requirements for Polysilicon Industryâ€. The government departments will strengthen industry supervision, promote comprehensive utilization of resources, and promote energy conservation and emission reduction. At the same time, industry enterprises should also strengthen self-discipline, and must continuously increase technology development, promote production cost reduction, promote product quality improvement, and reduce energy consumption and emissions. Establish product certification and monitoring systems to achieve standardized and standardized development of the industry. At the same time, improve the standards of related products, strict product quality, strengthen industry management, and establish the image of China's polysilicon industry. 3 Enhance the level of industrial technology and actively respond to international competition The expansion of global polysilicon production capacity has also brought tremendous impact pressure on China's polysilicon industry. From the domestic market point of view, the actual production of domestic polysilicon is still far less than the demand. However, foreign large companies use their technology and scale advantages to continuously lower prices, which has led to the influx of foreign polysilicon products into the Chinese market and crowding the domestic market. Oppress the market space of domestic polysilicon enterprises. According to customs statistics, China's polysilicon imports in September this year were 6,489 tons, up 0.24% from the previous month and up 52.9% year-on-year. Among them, China imported 1991 tons of polysilicon from South Korea, 1418 tons of polysilicon from the United States, and 1439 tons from Germany. From January to September, China's total imports of polysilicon reached 48,500 tons. On the one hand, the price of polysilicon continued to fall, and the actual transactions of domestic manufacturers became increasingly difficult. On the other hand, domestic polysilicon imports have hit record highs. The reason is that foreign polysilicon manufacturers rely on stable product quality and low price to attract domestic downstream manufacturers, and bind downstream enterprises to avoid risks through long-term contracts and high liquidated damages; second, because polysilicon prices are already lower than many domestic polysilicon. The production cost of enterprises, domestic polysilicon enterprises were forced to stop production and reduce production, resulting in a decline in domestic supply, forced to give up part of the market. Statistically, except for OCI's monthly export volume, the exports of WACKER, Hemlock and other companies to China have increased significantly in the past six months. At a time when the domestic market is not fully mature, mastering advanced technology is the best measure to deal with the crisis. Only by increasing technological innovation, storming technical difficulties, and effectively reducing production costs can we break the international monopoly. It is worth noting that a few of the domestic advanced polysilicon manufacturers represented by Jiangsu Zhongneng Silicon Industry are in the forefront of the industry through continuous technological improvement. According to the company's data, in the third quarter of 2011, its polysilicon production costs have dropped to about $20.9/kg, and it is expected to reach $20/kg through technical improvements by the end of 2011. For companies with low-cost manufacturing technology, price competition is not a problem, and even provides opportunities for such companies to integrate resources and expand production capacity. It turns out that only independent innovation and advanced production technology can be invincible in the competition. It can be predicted that small enterprises with backward technology and low competitiveness will be eliminated. In the market competition environment, the price of polysilicon will tend to be rational. The domestic polysilicon industry will gradually mature after adjustment. The advanced production technology with independent intellectual property rights is the key to the sustainable development of China's polysilicon industry.

Figure 5 The decline in domestic polysilicon production costs The environmental protection of domestic polysilicon production is also a major concern of enterprises and the community. Improved Siemens process polysilicon production in the process (such as chlorosilane synthesis, reduction, hydrogenation, etc.), will be accompanied by the production of large amounts of hydrogen, hydrogen chloride, trichlorosilane and silicon tetrachloride, the main by-product is silicon tetrachloride , hydrogen chloride, hydrogen, and high and low boilers. From the current situation of China's polysilicon industry, the use of polysilicon production by-products has become an important part of the large-scale production of polysilicon. There are many ways to treat by-product silicon tetrachloride. The effect of its outlet or comprehensive utilization is directly related to the economic benefits, energy consumption and environmental protection of polysilicon production, and even directly threatens the normal operation of polysilicon production line. Moreover, the recycling of silicon tetrachloride, hydrogen chloride and hydrogen in by-products is generally beneficial to reduce production costs. For the recycling of silicon tetrachloride, from the current layout of domestic enterprises, it is more suitable to use hydrogenation treatment, which is converted into trichlorosilane and reused, which not only solves the emission problem, but also improves the production of polysilicon. Out. At present, most of the domestic enterprises are mainly based on high-temperature hydrogenation, and they are also actively researching and applying low-temperature hydrogenation. The enterprises represented by low-temperature hydrogenation and hydrochlorination include Luoyang Zhongsi and Xuzhou Zhongneng. At present, polysilicon enterprises that have been put into production in China, such as Xuzhou Zhongneng, have solved the problem of full material circulation and clean production, and some are in the process of being solved, but the projects with a capacity of more than 1000t are basically equipped with silicon tetrachloride hydrogenation unit and hydrogen chloride and hydrogen. recycling system. At present, some enterprises have not yet achieved full-closed production, mainly through export, comprehensive utilization and pollution-free treatment. It is necessary to speed up the improvement and strengthen further technological upgrading. On the whole, the technical level of domestic enterprises is still uneven, and the pressure of energy conservation and emission reduction and cost reduction still exists. Faced with increasingly severe international competitive pressures, further reduction of production costs through technological innovation, transformation and upgrading is an important issue facing domestic polysilicon enterprises. Main problems and suggestions for the development of domestic polysilicon industry In the past few years, high-purity polysilicon preparation technology has been monopolized by foreign countries, resulting in scarcity of raw materials, and prices have remained high for a period of time, attracting a large influx of domestic funds and enterprises. Objectively Promoted the development of the domestic polysilicon industry. However, the recent silicon material market is sluggish, prices continue to fall, and the low-cost competition of foreign polysilicon enterprises continues to impact. The polysilicon enterprises that have just grown up in China are facing the challenges of internal and external troubles. Promoting technological progress with independent innovation of enterprises and accelerating product structure adjustment may help solve development problems. 1 Actively cultivate the domestic market, domestic demand drives industrial development. China is the world's largest producer of solar cells, and its battery output accounts for more than half of the world's total output. However, more than 95% of domestic PV products rely on export to European and American markets. Once the European and American markets fluctuate, they will affect domestic upstream enterprises. Serious dependence on external demand is a fatal injury to the development of the domestic PV industry chain. The growth rate of the European and American markets slowed down. The contradiction between the imbalance of supply and demand in the domestic PV industry was immediately highlighted, and there was a large backlog of inventory. The fierce price wars of various manufacturers have seriously weakened the profitability of Chinese enterprises. With the successive introduction and implementation of national golden solar engineering and concession bidding projects, the start-up speed of China's photovoltaic market is gradually accelerating. In 2010, China's new PV installed capacity was 500MW, and the cumulative installed capacity reached 800MW, nearly double the year-on-year. . In 2011, the National Development and Reform Commission issued and implemented a subsidy policy for on-grid tariffs for photovoltaic power generation. The photovoltaic market has grown substantially. It is expected that the installed capacity of new PV in China will reach 2.5GW, a year-on-year increase of 400%. According to another report, China's solar power generation "Twelfth Five-Year Plan" will also increase the 2015 PV installation target from 10GW to 15GW, and will reach 50GW in 2020. All kinds of good news show that China's PV market will accelerate and expand, and the digestive capacity of domestic PV production capacity will continue to increase. Then, through the industry consolidation, those low-competitive backward production capacity will be eliminated. By then, the domestic market share will increase rapidly. Relieve corporate pressure. 2 Strengthening the guidance of industry norms and promoting the industry's high profit, high subsidy and other industry advantages before the self-discipline development of the industry, so that a large number of enterprises are eagerly awaiting, although objectively promoting the rapid development of the industry, but under the influence of market fluctuations, the domestic polysilicon project has no The negative phenomenon of the preface is revealed. The volatility of the photovoltaic market and industry has provided an opportunity for the integration and upgrading of China's polysilicon industry. The Ministry of Industry and Information Technology has issued the “Entry Requirements for Polysilicon Industryâ€. The government departments will strengthen industry supervision, promote comprehensive utilization of resources, and promote energy conservation and emission reduction. At the same time, industry enterprises should also strengthen self-discipline, and must continuously increase technology development, promote production cost reduction, promote product quality improvement, and reduce energy consumption and emissions. Establish product certification and monitoring systems to achieve standardized and standardized development of the industry. At the same time, improve the standards of related products, strict product quality, strengthen industry management, and establish the image of China's polysilicon industry. 3 Enhance the level of industrial technology and actively respond to international competition The expansion of global polysilicon production capacity has also brought tremendous impact pressure on China's polysilicon industry. From the domestic market point of view, the actual production of domestic polysilicon is still far less than the demand. However, foreign large companies use their technology and scale advantages to continuously lower prices, which has led to the influx of foreign polysilicon products into the Chinese market and crowding the domestic market. Oppress the market space of domestic polysilicon enterprises. According to customs statistics, China's polysilicon imports in September this year were 6,489 tons, up 0.24% from the previous month and up 52.9% year-on-year. Among them, China imported 1991 tons of polysilicon from South Korea, 1418 tons of polysilicon from the United States, and 1439 tons from Germany. From January to September, China's total imports of polysilicon reached 48,500 tons. On the one hand, the price of polysilicon continued to fall, and the actual transactions of domestic manufacturers became increasingly difficult. On the other hand, domestic polysilicon imports have hit record highs. The reason is that foreign polysilicon manufacturers rely on stable product quality and low price to attract domestic downstream manufacturers, and bind downstream enterprises to avoid risks through long-term contracts and high liquidated damages; second, because polysilicon prices are already lower than many domestic polysilicon. The production cost of enterprises, domestic polysilicon enterprises were forced to stop production and reduce production, resulting in a decline in domestic supply, forced to give up part of the market. Statistically, except for OCI's monthly export volume, the exports of WACKER, Hemlock and other companies to China have increased significantly in the past six months. At a time when the domestic market is not fully mature, mastering advanced technology is the best measure to deal with the crisis. Only by increasing technological innovation, storming technical difficulties, and effectively reducing production costs can we break the international monopoly. It is worth noting that a few of the domestic advanced polysilicon manufacturers represented by Jiangsu Zhongneng Silicon Industry are in the forefront of the industry through continuous technological improvement. According to the company's data, in the third quarter of 2011, its polysilicon production costs have dropped to about $20.9/kg, and it is expected to reach $20/kg through technical improvements by the end of 2011. For companies with low-cost manufacturing technology, price competition is not a problem, and even provides opportunities for such companies to integrate resources and expand production capacity. It turns out that only independent innovation and advanced production technology can be invincible in the competition. It can be predicted that small enterprises with backward technology and low competitiveness will be eliminated. In the market competition environment, the price of polysilicon will tend to be rational. The domestic polysilicon industry will gradually mature after adjustment. The advanced production technology with independent intellectual property rights is the key to the sustainable development of China's polysilicon industry.

The development and problems of China's polysilicon industry

Recent Polysilicon Industry and Market Development Overview Polysilicon materials are the raw materials for semiconductor integrated circuits and solar photovoltaic cells. They are at the forefront of the information industry and renewable energy industry chain, with high production technology and large investment. In recent years, driven by the downstream solar photovoltaic industry and the semiconductor industry, especially the photovoltaic industry, the domestic polysilicon industry, market and technology levels have undergone great changes. With the development and changes of the international PV market, China is already the world's largest photovoltaic cell production base. From 2005 to 2008, the output growth rate of battery components exceeded 100%, and in 2008-2010, it exceeded 70%. In 2010, China's solar cell production exceeded 8.7GW (see Figure 1), among which four PV companies ranked among the top ten PV companies in the world. At the end of 2010, China's battery module production capacity exceeded 20GW, an increase of nearly 3 times compared with the same period of last year. It is expected that the production capacity will reach 35GW in 2011.